By Eman Zahra

By Eman Zahra

The distinction that destroys revenue cycles isn’t a billing error. It’s a misclassification — the silent moment when a payment poster treats an insurer’s $80 payment on a $120 allowed claim as a contractual write-off instead of an underpayment requiring dispute. That $40 disappears. Multiplied across 500 claims per month, it’s $240,000 in annual revenue written into oblivion.

MGMA benchmarks document this consistently: practices lose between 3% and 7% of gross revenue annually from underpayments and incorrect adjustments. For a $3 million practice, that’s $90,000 to $210,000 — recovered by no one, discovered by no audit, attributed to no error.

The core operational failure isn’t ignorance of payer contracts. It’s the failure to distinguish three discrete financial events that look identical on a remittance: a valid contractual adjustment, a payer underpayment requiring dispute, and a legitimate patient balance. Conflating them violates payer contracts, risks False Claims Act exposure, and permanently removes recoverable revenue from the books.

What Legally Separates a Valid Patient Balance From Prohibited Balance Billing?

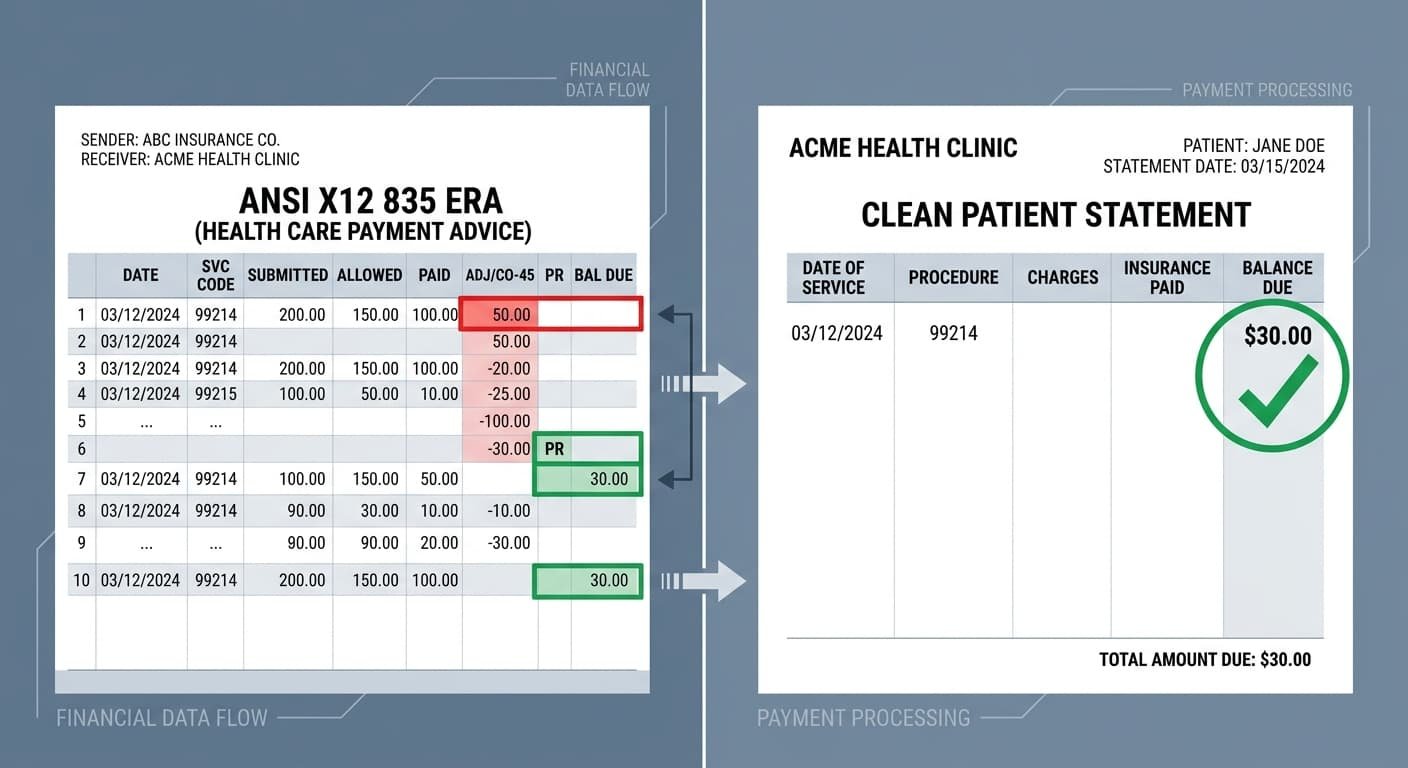

A valid patient balance consists exclusively of amounts designated under the PR (Patient Responsibility) group code on the ANSI X12 835 Electronic Remittance Advice: deductibles, copayments, and coinsurance. Billing patients for amounts designated CO (Contractual Obligation) — including amounts the payer underpaid relative to the contracted fee schedule — constitutes prohibited balance billing under in-network provider agreements.

That distinction is non-negotiable once a provider signs an in-network contract. The agreement establishes that the contracted allowed amount represents payment in full for covered services. The insurer’s adjudicated portion plus the patient’s cost-sharing equals that allowed amount — not a dollar more.

The No Surprises Act (effective January 1, 2022) extended these protections federally into emergency and certain non-emergency contexts involving out-of-network providers at in-network facilities. (See CMS No Surprises Act enforcement framework) Penalties for violations reach $10,000 per incident, and CMS has confirmed active enforcement tracking. Patient complaints filed through the federal feedback portal had already generated $3 million in monetary relief to consumers through October 2023.

What competitors consistently mischaracterize is the operational trigger: the ERA group code. CO designates amounts the provider contractually agrees not to collect — from anyone. PR designates amounts adjudicated as the patient’s contractual share. Only PR-coded balances belong on a patient statement. Posting CO-coded amounts to the patient account isn’t a collection mistake; it’s a compliance violation that distorts AR, generates payer audits, and exposes the practice to OIG scrutiny.

How Do CO and PR Group Codes on the ERA Determine Patient Liability?

On the ANSI X12 835 ERA, the CO (Contractual Obligation) group code identifies amounts waived under the provider-payer contract, including the CO-45 adjustment for charges exceeding the fee schedule. The PR (Patient Responsibility) group code identifies deductible, copay, and coinsurance amounts the patient legitimately owes. Only PR-coded line items transfer to patient statements.

CARC CO-45 is the single most frequently misposted code in revenue cycle operations. It signals that the payer paid less than the billed charge because the contracted rate is lower — not that the payer made a payment error. The problem emerges when the payer actually remits below the contracted rate. That scenario generates no distinguishing CARC. It looks identical to a valid CO-45 adjustment on the surface.

This is the underpayment trap. A payment poster sees $100 paid on a $180 charge, posts CO-45 for $80, and closes the claim. If the contracted rate for that CPT code is $130, the payer shortchanged the practice by $30. That $30 isn’t a contractual write-off — it’s a payer error demanding dispute. Without active fee schedule crosswalk verification, it becomes a permanent write-off instead.

The CY 2026 CMS Physician Fee Schedule Final Rule (effective January 1, 2026) established two separate conversion factors for the first time: $33.57 for qualifying APM participants and $33.40 for non-qualifying participants, both increases from the 2025 rate of $32.35. (CMS PFS CY 2026) Practices using Medicare-indexed payer contracts that haven’t updated their fee schedule crosswalk to reflect these 2026 figures are benchmarking every variance calculation against the wrong denominator.

The 2.5% efficiency adjustment to work RVUs for non-time-based services, also introduced in the CY 2026 rule, compounds this. An outdated crosswalk doesn’t just produce slightly inaccurate numbers — it systematically misclassifies legitimate underpayments as acceptable CO-45 write-offs across every affected CPT code, every claim, every month.

What Happens When the Payer Underpays—Is the Patient the Right Collection Target?

When a payer pays below the contracted allowed amount, the correct collection target is the payer — not the patient. In-network providers cannot shift underpayments to patients under contract terms. The appropriate action is a payer underpayment appeal with ERA documentation, fee schedule evidence, and contract rate comparison — initiated before writing off any balance.

This is where most RCM workflows collapse. Underpayment appeals require three operational inputs most practices don’t maintain at the line-item level: a current payer-specific fee schedule loaded into the practice management system, a systematic ERA-versus-contract comparison triggered on every remittance, and a documented escalation path with internal deadlines that precede the payer’s external appeal window.

Payer contracts typically impose 90- to 180-day windows for underpayment disputes — sometimes shorter for specific commercial plans. Missing those windows converts a recoverable underpayment into a permanent write-off. The practice didn’t lose that money to contractual obligation; it lost it to clock management failure.

The operational fix requires treating post-payment review and payment posting as separate functions with separate accountabilities. Payment posters close claims. Underpayment analysts dispute them. Collapsing these functions into a single role is the root cause of the 3–7% annual revenue leakage MGMA documents year after year.

How Should the Payer Appeal Be Structured Before Touching the Patient Account?

A compliant payer underpayment appeal must include: the original claim with CPT and ICD-10 codes, the ERA with the relevant CARC/RARC codes, the applicable fee schedule section from the provider-payer contract, and a line-item variance calculation. Most commercial payers require written appeals within 90 to 180 days of the original remittance date.

The appeal letter must cite the specific contract language governing the disputed CPT code, the contracted rate, the paid amount, and the calculated variance. Generic “we believe this was underpaid” language fails consistently. Specific, documented variance calculations force reconsideration and build the paper trail required if the dispute escalates to state insurance commissioner complaint or binding arbitration.

Practices implementing systematic variance reporting — comparing ERA payments against payer-loaded fee schedules at the claim line level — recover $80,000 to $200,000 annually in previously abandoned balances, according to RCM operations data. That revenue was already earned, already documented, already billed. It simply required someone to claim it before the window closed.

Which Financial Policies Legally Protect Patient Balance Collection?

A legally compliant financial policy must specify: the basis for patient balance calculation (PR group code from ERA), the timeline for patient statements, the process for financial hardship applications, and the prohibition on balance billing beyond contracted patient responsibility. Patients must sign the financial policy at registration. Credit card on file programs require separate written authorization.

The OIG has established with clarity that routine copay and deductible waivers — even when informally applied to offset underpayment frustration — trigger Anti-Kickback Statute risk under 42 U.S.C. § 1320a-7b(b). (OIG Fraud & Abuse Laws) The only defensible waiver ground is documented, individual financial hardship assessed through a consistent, written, needs-based process. Systematic waiver patterns, even when applied case-by-case without formal policy, create False Claims Act exposure under 31 U.S.C. §§ 3729–3733.

This creates a genuine operational tension. The practice is underpaid by the insurer. The patient legitimately owes the contractual PR balance. Billing staff face pressure from both directions. The answer isn’t to waive the patient’s legitimate PR balance to compensate for insurer shortfall. The answer is to pursue the payer dispute aggressively while simultaneously collecting only the PR-designated patient responsibility — two parallel workflows, not sequential choices.

Advance Beneficiary Notices govern a specific and often mishandled subset of this problem: traditional Medicare patients facing potential medical necessity denials. An ABN must be signed before service delivery, not after denial. Without a valid ABN, the provider cannot bill the patient for the denied amount regardless of what appears on the remittance. This requirement does not automatically extend to Medicare Advantage plans, which operate under separate patient liability frameworks — a distinction that generates disproportionate billing errors in practices serving mixed Medicare populations.

What Are the Direct Legal Risks of Improper Patient Balance Collection?

Billing patients for CO-coded amounts — or collecting from patients before exhausting payer dispute rights — risks: payer contract termination, state insurance commissioner complaints, False Claims Act liability for any government program patients affected, Civil Monetary Penalties up to $10,000 per NSA violation, and Anti-Kickback Statute exposure from compensatory copay waivers applied to offset collection shortfalls.

The CMS Final Rule on Medicare Overpayments, effective January 1, 2025, replaced the prior “reasonable diligence” standard with the FCA “knowing” standard. Providers who knowingly retain overpayments — which can result when incorrect patient overcollection generates a refund obligation — now face a formalized 180-day investigation clock before the 60-day return deadline triggers. Missing that window converts a compliance issue into potential treble-damage FCA liability.

OIG exclusion remains the existential risk in this space. An excluded provider cannot bill Medicare, Medicaid, or any federal program — effectively ending participation in the two largest payer pools in most practices. Exclusion authority under 42 U.S.C. § 1320a-7 applies to systematic false billing patterns, and that includes patterns of improper patient balance collection that affect government program beneficiaries at scale.

The collection path is operationally clear. Verify every ERA line against the contracted fee schedule before posting any adjustment. Route underpayments to dispute — not write-off. Collect only PR-designated balances from patients. Document every hardship waiver individually with needs-based evidence. Run payer variance reports monthly, not at contract renewal. Practices that follow this sequence don’t write off recoverable revenue. They collect what the contract authorizes and appeal everything it guarantees.

This article is intended for healthcare revenue cycle professionals, practice managers, and compliance officers. It does not constitute legal advice. Consult qualified healthcare counsel for jurisdiction-specific guidance on payer contract interpretation and patient billing compliance.

Leave a Reply